Rising government bond yields have contributed to a sell-off by the pandemic high-fliers in the stock market, but is unlikely to be enough to spoil the appeal of equities over bonds in 2021, according to one analyst.

US equity investors “have focused on the recent rise in 10-year government bond yields in the past week, going all the way back to mid-February 2020,” wrote Lori Calvasina, head of US equity strategy at RBC Capital Markets. in a Tuesday note. Yields and bond prices have an inverse relationship.

The 10-year Treasury proceeds TMUBMUSD10Y,

is experiencing its largest rise in six weeks, causing a relapse led by technology-focused stocks that had benefited most from the stay-at-home dynamics created by the COVID-19 pandemic.

Related: Can the equity bull market survive rising inflation and bond yields? This is what history says

The relationship was seen in reverse on Tuesday as interest rate hike eased following testimony from Federal Reserve Chairman Jerome Powell, allowing key benchmarks to wipe out or curtail significant losses. The technically demanding Nasdaq Composite COMP,

which led the way down, a loss of nearly 4% limited to 0.5% as revenues fell; the S&P 500 SPX,

made a profit to make a five-day loss series, while the more cyclical-oriented Dow Jones Industrial Average DJIA,

a loss of more than 360 points to finish a little higher.

Meanwhile, Calvasina said a look at what stocks have to offer in terms of dividends and earnings yield versus bonds, and a reminder of what kind of bond moves have caused problems for stocks, provides some reassurance that 2021 is unlikely to turn into a downward , she said.

Dividend Yield

When it comes to dividend yield, RBC has measured the percentage of companies that continue to exceed yield on 10-year Treasury bonds. While that dropped from 64% to 51.5% at the start of the year, it’s still within a range typically followed by a 17% gain for the S&P 500 over the next 12 months, she said.

Profit Yield

The earnings yield of the S&P 500 has also deteriorated, moving towards the lower end of the bandwidth since the end of the financial crisis. It is now close to the 2017-18 level, but remains within a range that was followed by 9.3% average gain by the S&P 500 over the next 12 months, Calvasina said.

In other words, this analysis acknowledges the arguments for a short-term pullback in the S&P 500, but does not necessarily mean that investors should move to the exit in the longer term, ”she wrote.

Calvasina also highlighted a “key difference” between 2018, when the trade war threatened the US and the world economy, and now, when forecasts for gross domestic product are rising rapidly.

Treasury yields and shares

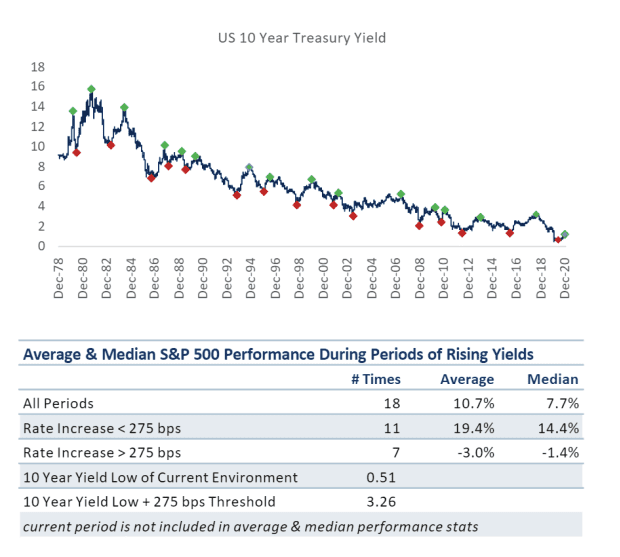

Finally, what about the rise in interest rates on Treasury bonds themselves? Indeed, many market observers have argued that while returns remain low by historical standards, the magnitude of the rise may be of greatest concern to equities. Calvasina has broken down the relationship between interest rate movements and stock market performance in the chart below:

RBC Capital Markets

Calvasina said US stocks tend to struggle if 10-year yields rise more than 275 basis points or 2.75 percentage points. Hitting the low of 0.51%, a move of 275 basis points would bring returns to around 3.26%. The 10-year ended Tuesday at 1.363%.